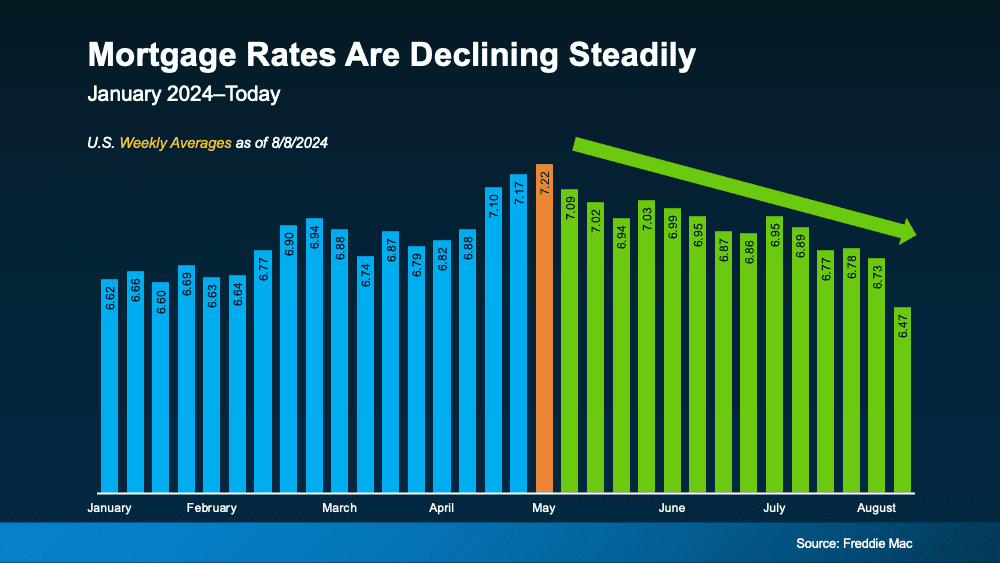

If you're considering a home purchase this year, your focus is likely on mortgage rates. As these rates directly impact your affordability when securing a home loan, it's crucial to gain insight into their historical context and their relationship with inflation. Let's explore where mortgage rates have been, where they stand today, and what the future might hold.

Putting Today's Rates in Perspective

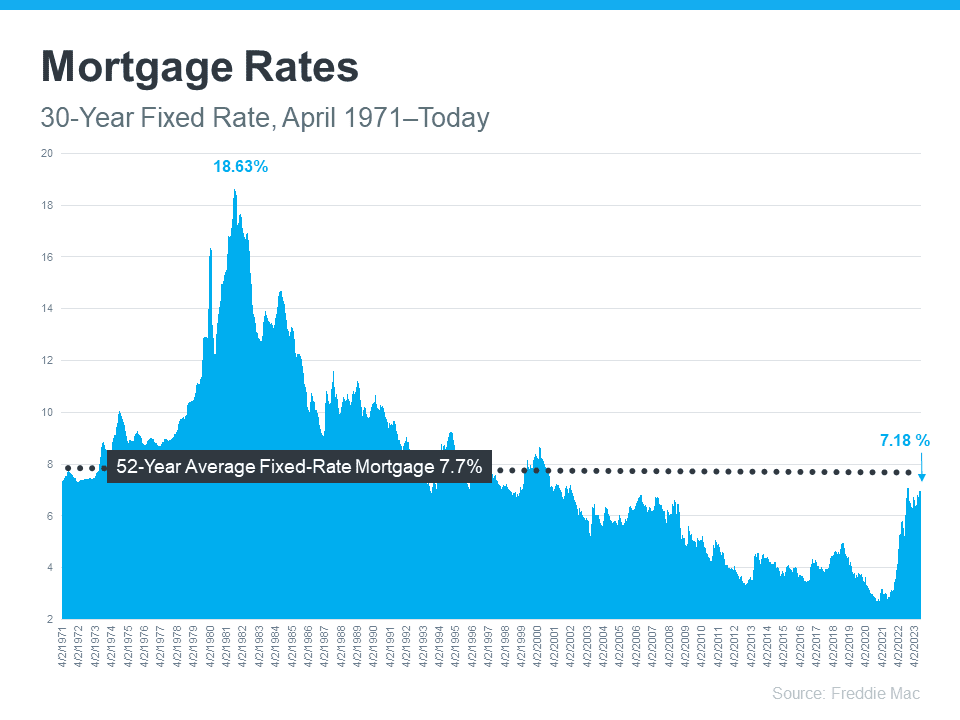

Freddie Mac has meticulously tracked the 30-year fixed mortgage rate since April 1971. Their Primary Mortgage Market Survey compiles mortgage application data from lenders nationwide, offering valuable insights (see graph below):

The right side of the graph shows a significant increase in mortgage rates since the beginning of last year. However, when viewed within a historical context, today's rates remain below the 52-year average. While this perspective is reassuring, it's essential to remember that many buyers have grown accustomed to rates ranging between 3% and 5% over the past 15 years.

This familiarity explains why the recent rate uptick might feel like a shock, even though rates are relatively close to their long-term average. For many buyers, a slightly lower rate would be welcome. To assess the likelihood of this scenario, we need to consider the role of inflation.

Examining the Future of Mortgage Rates

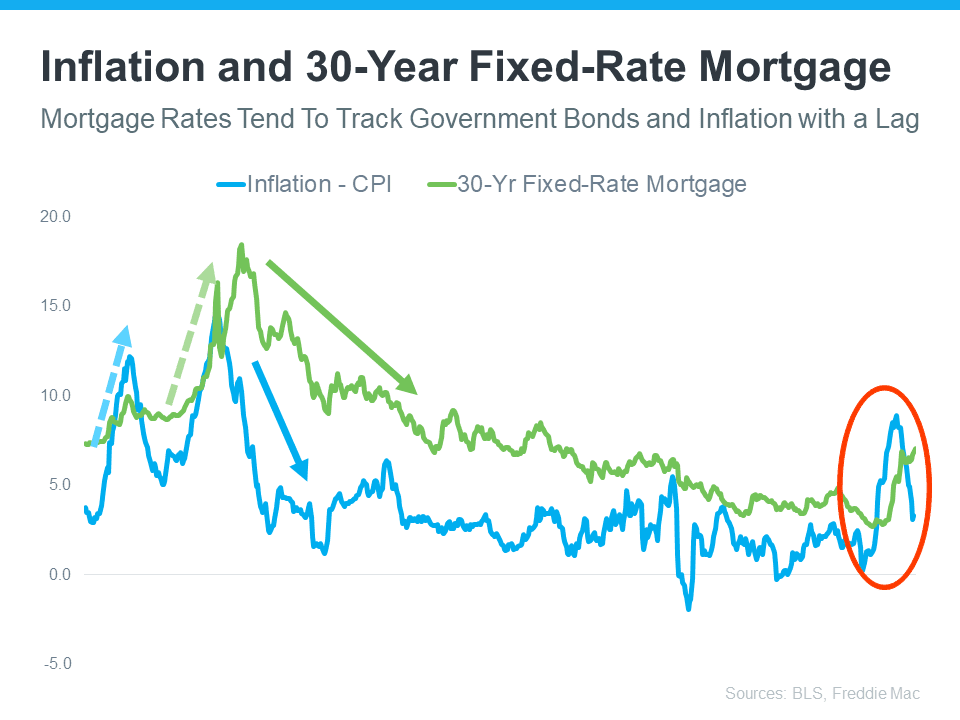

Since early 2022, the Federal Reserve has been diligently working to curb inflation. Historically, inflation and mortgage rates have shared a notable connection (see graph below):

The graph illustrates a consistent relationship between inflation and mortgage rates. Observing the left side of the graph, whenever inflation experiences significant changes (indicated in blue), mortgage rates tend to follow suit shortly afterward (indicated in green).

The circled portion of the graph highlights the recent surge in inflation, closely trailed by a rise in mortgage rates. While inflation has somewhat moderated this year, mortgage rates have yet to reflect a similar adjustment.

Following this historical pattern, it's plausible that mortgage rates will soon align with the decreased inflation. Although predicting precise rate movements is challenging, the current trend suggests potential improvements in mortgage rates, offering optimism for aspiring homeowners.

In Conclusion

To anticipate future mortgage rates, it's valuable to assess their historical trajectory. The established link between inflation and mortgage rates suggests that the recent decline in inflation could bode well for prospective homebuyers. For a comprehensive understanding of your mortgage rate outlook and homeownership prospects, reach out to me, Anthony Spitaleri at Serhant, your trusted real estate professional.