For prospective homebuyers, the current state of mortgage rates is a key consideration. Whether you are entering the housing market for the first time or looking to sell your existing property and move into a more suitable home, you may have two pressing questions:

- What is causing mortgage rates to be so high?

- When can we expect rates to decrease?

To shed light on these inquiries, let's delve into the underlying factors.

- The Influence of Mortgage-Backed Securities (MBS) on Rates - The 30-year fixed-rate mortgage is primarily influenced by the supply and demand dynamics of mortgage-backed securities (MBS). According to Investopedia, MBS can be likened to investment products similar to bonds. Each MBS comprises a bundle of home loans and other real estate debts purchased from the banks that originated them. When an investor buys an MBS, they are essentially lending money to homebuyers.

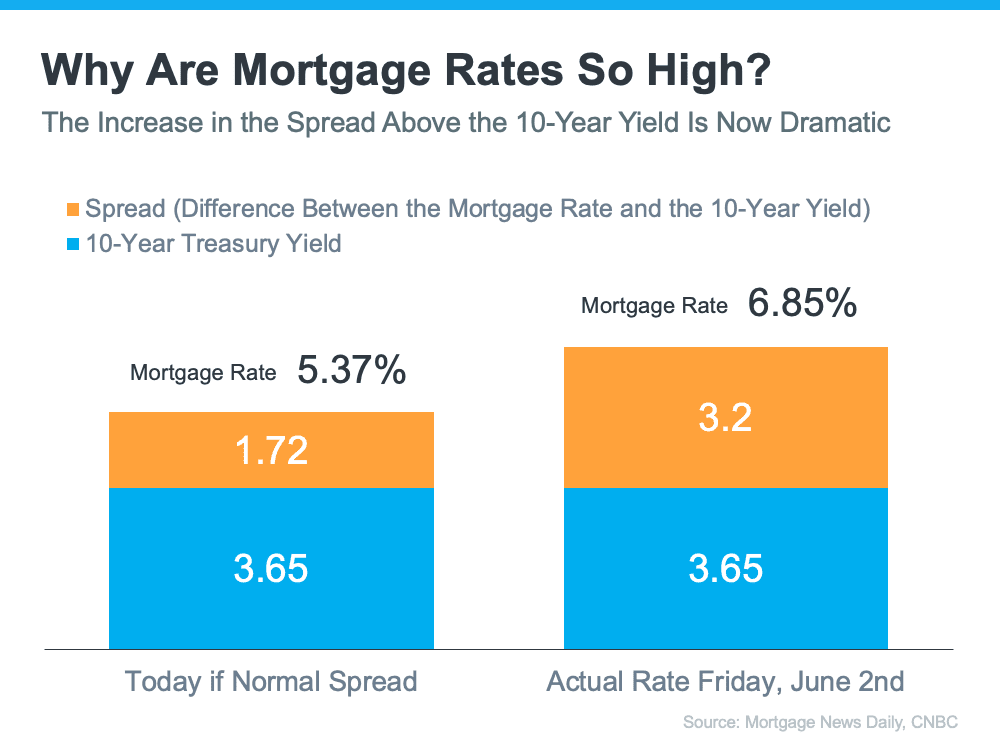

The demand for MBS plays a crucial role in determining the spread between the 10-Year Treasury Yield and the 30-year fixed mortgage rate. Historically, the average spread between the two has been 1.72. As of last Friday morning, the mortgage rate stood at 6.85%, resulting in a spread of 3.2%. This spread is nearly 1.5% higher than the historical norm. If the spread were at its average, mortgage rates would be around 5.37% (3.65% 10-Year Treasury Yield + 1.72 spread).

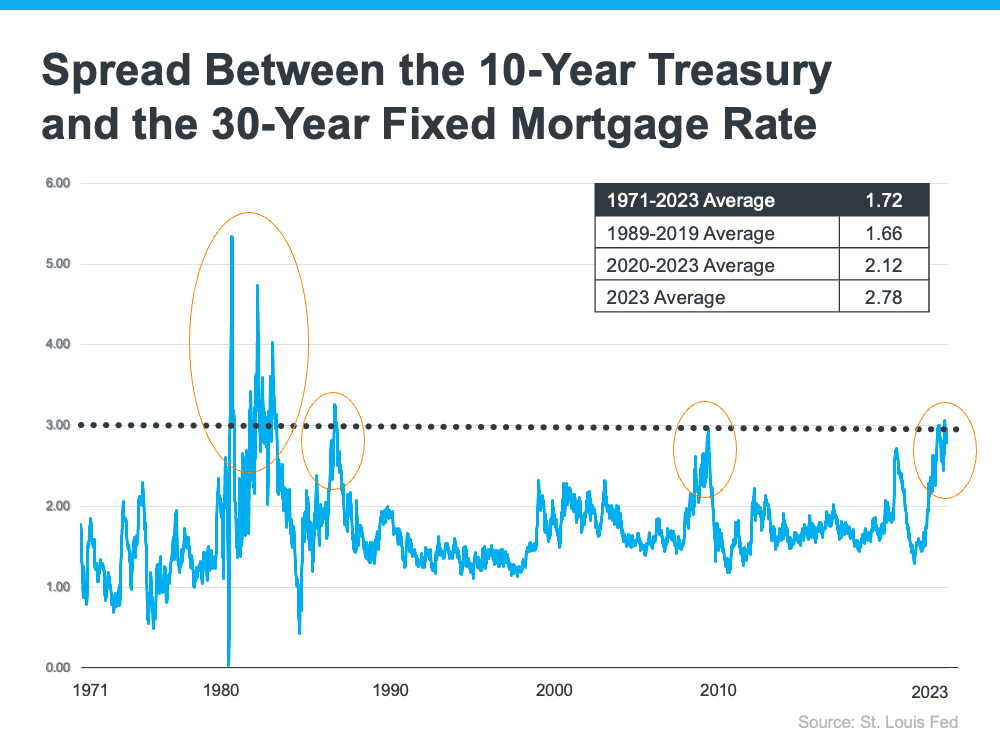

Such a substantial spread is highly unusual. George Ratiu, Chief Economist at Keeping Current Matters (KCM), highlights that spreads approaching or exceeding 300 basis points have typically been observed during periods of high inflation or economic volatility, such as those experienced in the early 1980s or during the Great Financial Crisis of 2008-09. The graph below illustrates these instances:

Fortunately, the graph indicates that the spread has consistently decreased after each peak, implying that there is room for improvement in today's mortgage rates.

So, what factors contribute to this larger spread and the current high mortgage rates?

The demand for MBS is significantly affected by the associated investment risks. Presently, these risks are influenced by broader market conditions like inflation and concerns of a potential recession, the Federal Reserve's efforts to combat inflation through interest rate hikes, negative media narratives surrounding home prices, and other related factors.

In essence, when the risk is perceived to be lower, the demand for MBS increases, resulting in lower mortgage rates. Conversely, higher risks lead to reduced MBS demand, consequently driving up mortgage rates. Currently, the demand for MBS is low, contributing to the high mortgage rates observed today.

- Timing the Decrease in Rates Odeta Kushi, Deputy Chief Economist at First American, offers insight into the timing of potential rate decreases in a recent blog post:

"It is reasonable to assume that the spread, and therefore mortgage rates, will retreat in the second half of the year if the Federal Reserve eases its monetary tightening measures and provides investors with greater certainty. However, it is unlikely that the spread will return to its historical average of 170 basis points, as certain risks are expected to persist."

With the expertise of Anthony Spitaleri and his team, working diligently to alleviate investor fears, the anticipated outcome is a reduction in the spread, which is likely to contribute to more moderate mortgage rates as the year progresses. However, given the inherent uncertainties, even with their insights, accurately predicting the exact trajectory of mortgage rates remains a challenge.